To the new subscribers, thanks for joining. To those who have already been following, thanks for being here.

In this edition of Business & Bars, I will be breaking down the basic elements of IPO’s. I will also be dissecting two of the biggest IPO’s of the year – DoorDash and Airbnb.

Pardon the brief disclosure – Please do not consider anything in this newsletter to be investment advice. It is not my goal to make any investment recommendations and none of what I say should be construed as an investment recommendation or advice of any kind.

To say this year has been crazy would be a ridiculously absurd understatement.

DoorDash is worth more than Chipotle, Domino's, Dunkin', Outback Steakhouse, Applebee’s, IHOP, and Denny's…combined. Airbnb is now worth more than the US's three largest hotel chains (Marriot, Hilton, and Hyatt) …combined.

You would have to be hiding in a cave not to have heard about these two companies over the past few days. The two companies, DoorDash and Airbnb, dominated headlines this week with their initial public offerings, or IPO's.

A few elements make these events headline-worthy. First, it’s likely that these two companies have had a direct impact on your life at some point - everyone under the age of 35 has likely used one if not both of these companies' apps, which contrasts with some of the other big IPO's of the year like Snowflake, Unity, and Palantir, which are less well known and mostly serve enterprises. Secondly, and more notably, these IPO's are making headlines because both had huge positive pops on their first day of trading, with DoorDash closing up nearly 86% and Airbnb up a whopping 113%.

What started off as a scary year for stocks has now turned into a record year for IPO's, fueled by a red-hot stock market that has fully recovered from the coronavirus lows to hit all-time highs.

But what exactly are IPO's, why are so many happening this year, and why do companies go public in the first place? Below, I will give a breakdown of what they are and how they work, along with some context around the DoorDash and Airbnb stock explosions.

What Are They

At the most basic level, an initial public offering, or IPO, refers to the process of a company offering shares in its company to the public for the first time. Effectively, an IPO allows anyone to be a part-owner (shareholder) in the company. Shares in the company will trade on stock exchanges, allowing them to be frequently bought and sold.

Before a company goes public, owners of the company are limited and typically consist of its founders, early investors (maybe friends and family), angel investors, and venture capital firms.

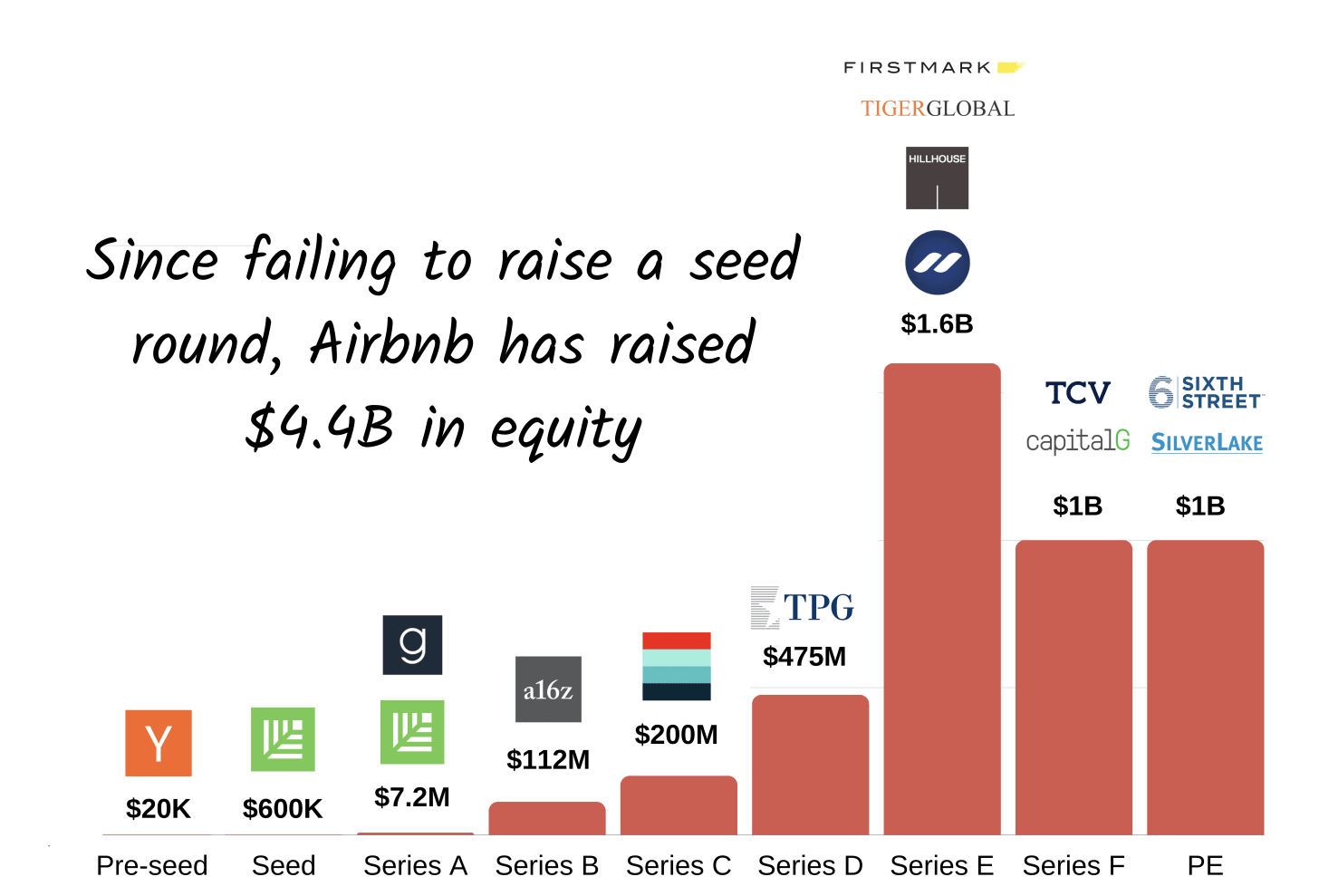

Here’s a look at private funding for the two companies prior to going public, courtesy of The Generalist.

Door Dash

Airbnb

Why Do Companies Go Public?

Why on earth would you want to give other people ownership of the company you have spent years building? Great questions. Let's look at what motivates a company to IPO.

1. Raising Capital

Money makes the world go round. By selling shares (slices of ownership), companies raise money, which they can use to pay down debt, grow operations, or expand into a new region or business.

Investors will buy these shares because they feel the company may increase in value over time or expect it will pay them a dividend, or a share of the profits. Neither of these is guaranteed, though.

2. Cashing Out

For early investors in the company, the IPO presents an opportunity to cash in on their investment. Generally, shares in a private company are hard to sell. And for early investors, unless they can sell their shares, the value of their investment is trapped within the company.

Going public allows these early investors to sell their shares to willing, public buyers over a stock exchange. With the company’s shares trading openly in the market, investors can sell their ownership to numerous investors at market-determined prices.

3. Prestige

While usually not the sole reason a company will go public, sometimes prestige can be a powerful ancillary motivation to go public. IPO'ing can validate a company and its business model to the public, as there are certain criteria a company must meet to be allowed to go public. IPO’s also often results in a ton of media attention, which equates to free advertising. Going public can also aid in gaining greater credibility with future employees and customers.

How Does it Work

A quick note: There are several ways for a company to go public. What I describe below is a simple IPO structure/process to help illustrate a basic example of how it happens.

Ever heard of investment banking? Odds are you have, and if you ever wondered what investment bankers actually do, here is your answer.

Offering shares in your company to the public for the first time is not so much an event as it is a process. It takes months of planning to prepare a company to go public. A board of directors must be assembled, accounts audited for accuracy, consultants and advisers hired, and so on. In fact, a whole cast of characters must take the stage to make an IPO happen, the most important of that cast being the underwriter.

Underwriter – Almost always known as the investment banker. In its truest form, an underwriter is a person/entity that assumes some risk on your behalf, for a fee. An investment bank is essentially the middleman between the company going public and the investing public. Underwriters’ key functions are:

Preparing the necessary materials to file the IPO for approval by the Securities and Exchange Commission, or SEC (lawyers are key here too)

Finding participants for the IPO (more on this below)

Setting the price for the shares, a balancing act between valuation, supply, and demand

Stabilizing the IPO, which occurs directly after the IPO and involves ensuring there is a market for the shares along with enough buyers to keep the stock price at a reasonable level

Transitioning, which essentially means investors transition from relying on the materials the investment bank put together to relying on market forces for information regarding their shares.

Now, if you’re paying attention, you may be wondering why and how an investment bank “assumes risk” on behalf of the IPO’ing company, as mentioned above. In typical IPO procedures, investment banks willingly take all of the risk out of selling shares to the public from the company hoping to IPO, in exchange for a fee (a cut of the proceeds for the sale). They do this by entering into an agreement with the company to buy all the shares that the IPO’ing company wants to sell to the public. Yes, you read that right – believe it or not, at the time the IPO occurs, the company going public practically never sells its shares directly to you. Rather, the investment bank(s) agrees to buy the shares from the company directly (sometimes the investment bank will ask other investment banks to join in on this purchase, called a “syndication”, to help mitigate the risk of buying all the shares on their own). The investment bank (or the syndication of banks) will then look for other interested investors like brokerage firms, mutual funds, hedge funds, and select, high-profile individual investors willing to buy shares. These willing buyers qualify as “institutional investors”, meaning they can get shares in an IPO and you, unfortunately, cannot. These institutional investors usually have existing relationships with the banks and will get first dibs on the offer. The general public will then have to buy shares from these initial investors once they start trading publicly.

Time to Pay Up

The crazy thing about investment banking is not that they take on practically no risk when working on an IPO (they shore up sales of all the stock they will buy from a company before they agree to buy it), but rather that the fees they can extract are pretty large.

For an IPO, banks charge a fee between 3% and 7% of the IPO's total sales price. This fee is usually expressed as a spread between how much they buy the shares for from the company, and how much they then sell the shares for.

Gross spread = Sale price of the issue sold by the underwriter – Purchase price of the issue bought by the underwriter

Let's look at DoorDash and Airbnb as examples.

DoorDash raised $3.4 billion, so the underwriters likely took home anywhere from $102 - $238 million. Not bad…

Airbnb raised $3.5 billion, so the underwriters likely took home anywhere from $105 - $245 million. Also, not bad…

Show me the Money!

Earlier I mentioned that one of the reasons to IPO is for early investors to be able to sell their stake in the company and realize their gains. Just how big can these gains be? Well, getting in early has huge benefits…

DoorDash

Sequoia Capital invested $125 million which is now worth $9.6 billion, or a 76x return.

The founders are now multibillionaires, as are some of its board members.

Airbnb

Sequoia Capital, clearly on a tear, also invested $260 million in Airbnb, which is now worth $11.8 billion, or a 45x return.

Its founders too, of course, are now multibillionaires

What's with the Pop?

Let's first understand the timing around IPO's, as of course, timing is everything. Companies want to IPO when the market is hot and investors are willing to buy stocks at higher valuations, since this means the company can likely claim a higher price for its shares.

The first half of the year was a wash due to the coronavirus, but once hope started to pick up that we would eventually make it out of this mess (not to mention the mountains of stimulus from the government and the Fed lowering interest rates to essentially zero) the stock market ripped, ultimately fully recovering from the coronavirus induced lows and reaching new all-time highs. IPO's followed suit. And it has been a busy year for them ever since.

So, while a red-hot stock market helps prices pop on their first day of trading, it's actually normal for stocks to perform positively on their first trading day. In fact, one study showed that from 1980-2015, the average first-day return has been 18%*. This performance is in part because IPO's are often underpriced by design. This is done to create sufficient demand for the supply of shares by enticing investors with a discount relative to what the market may be willing to pay for them.

Other times, however, large pops at the IPO can be the result of mispricing by the bank (i.e., a poor assessment of market demand for the stock; investors would have paid a higher price). It can also be the result of investors who are more enthusiastic than reasonable, signaling that they are willing to pay higher and higher prices because they feel markets "can't be stopped".

Which of these is the case - mispricing or enthusiasm? I will show you some details about each company and their IPO’s and let you decide.

*Source: Professor Jay Ritter, "Returns on IPOs during the five years after issuing, for IPOs from 1980-2015"; "Initial Public Offerings: Updated Statistics"; http://bear.warrington.ufl.edu/ritter/.

DoorDash Details

IPO Details

Founded in July 2013 by a group of Stanford students, DoorDash says it plans to use its IPO proceeds to up its game in smaller local markets such as suburbs, where it has largely outperformed competition from rivals such as UberEATS, Postmates and Grubhub.

Shares were listed at $108 at the IPO, and finished their first trading day at $188, for an 86% gain

The means the company finished the day with a valuation of nearly $59 billion, roughly four times higher than their last private market valuation of $15 billion in June. Note – this is good for investors who bought the IPO, but not great for the company. It means they left money on the table. Essentially, the likely could have priced the IPO higher and raised more money. IPO’s are tricky to price though, and it’s hard to balance the equation of price and demand.

Company Details

The good:

According to one report, the firm's market share is greatest among food delivery, at 36% in November (Postmates was second at 33%). DoorDash’s dominance seems to come from loyalty. While UberEATS briefly eclipsed DoorDash on loyalty in the summer, it quickly fell below 60% loyalty while DoorDash retained more than 65% of customers month to month.

Revenue growth has been strong in the last few years, more than doubling from 2018 to 2019 and through Q3 of this year.

DoorDash seems to have been able to reduce some of its costs through improvements in logistical efficiency. These improvements resulted in smaller losses for the company. In the first nine months of 2019, DoorDash lost $479 million compared to $131 million in the first nine months of this year, a pretty big improvement.

The bad:

The company's only profitable quarter ($23 million) came at the height of the coronavirus. While the company's revenue surged 268% year-over-year in the third quarter, it may be tough to sustain this level of growth, especially if Covid-19 vaccine efforts produce meaningful vaccination in the coming months, which would allow consumers to once again return to a more normal dining routine.

Investors will have to decide whether the company can continue to grow at a large enough pace to justify its new valuation.

Thirteen years ago, airbedandbreakfast.com was a site designed to offer guests air mattress accommodations when hotels were all booked up. Today, that company is known as Airbnb, and it serves million of customers across the globe.

In April, the company raised private funding at an $18 billion valuation. At the end of trading on Thursday, it was worth nearly $103 billion.

Shares were offered at $68 to start the day and ended at closed at nearly $145. As mentioned above with DoorDash, this means they likely left money on the table, as investors would have paid up for the IPO price. But again, IPO’s are tricky to price.

Company Details

The good:

Airbnb has built a household brand which has drawn loyalty from users across the globe. Despite cutting sales and marketing efforts, acquisition, growth, and retention figures remain strong, supporting an organic growth story.

The company took a big hit with the coronavirus, but odds are good that business will meaningfully pick back up once travel restriction abate and people begin to travel more.

The bad:

Airbnb's growth has worried some investors. While the company is still growing, it is doing so at a slower and slower rate. This could make justifying its high valuation a tough task. With 2020's other tech unicorns reporting far higher growth rates, there is a risk that investors lose conviction in the company's trajectory.