The 10 Financial Commandments...Explained

I wrote a rap remixing a Biggie classic, "The 10 Crack Commandments", and adapted it to apply to something more productive - personal finance. Below I break these principles down.

My motivation for writing this song is that I feel the majority of Americans don't receive proper education on basic financial concepts that have the potential to increase their quality of life. And let's face it, finance can be boring...so I figured a song and music video are a better format to present the information. Below I expand upon the commandments discussed in the song to give listeners a better understanding of what they mean.

Number 1. Emergency Fund

What is it? In simple terms, it's money you set aside for the financial surprises life inevitably throws at us. It's important because while we all have expenses that are of a set amount and schedule, like rent, car payment, phone bill, etc., no one can predict when they might lose their job and no longer earn income to cover their bills, or when they might get sick and have medical bills which they can't cover with their wages alone.

How much should I save? Typically, you should aim for at least 3 - 6 months' worth of expenses saved. This varies of course by each person and their scenario.

You are not alone! It's never too late to get started. 56% of people in the United States don't have a rainy day fund that would cover 3 months of expenses, which highlights how truly unappreciated this concept is (Source: FINRA Investor Education Foundation National Financial Capability Study, 2012).

Where should I keep my emergency fund? 2 options - 1) a savings account or 2) a money market fund. A money market fund is simply is an investment vehicle that invests in cash-like investments, which are very low risk and can offer more interest than a savings account. Stocks, for example, aren't a good place to put your emergency funds, since they can change widely in value. You want to make sure this money is there when you need it.

Keep it separate! Simple but important - keep your emergency fund separate from your checking account so you're not tempted to use it for non-emergency purchases…those new shoes can wait! (more on this under Number 7).

2. Number 2. Compound Interest

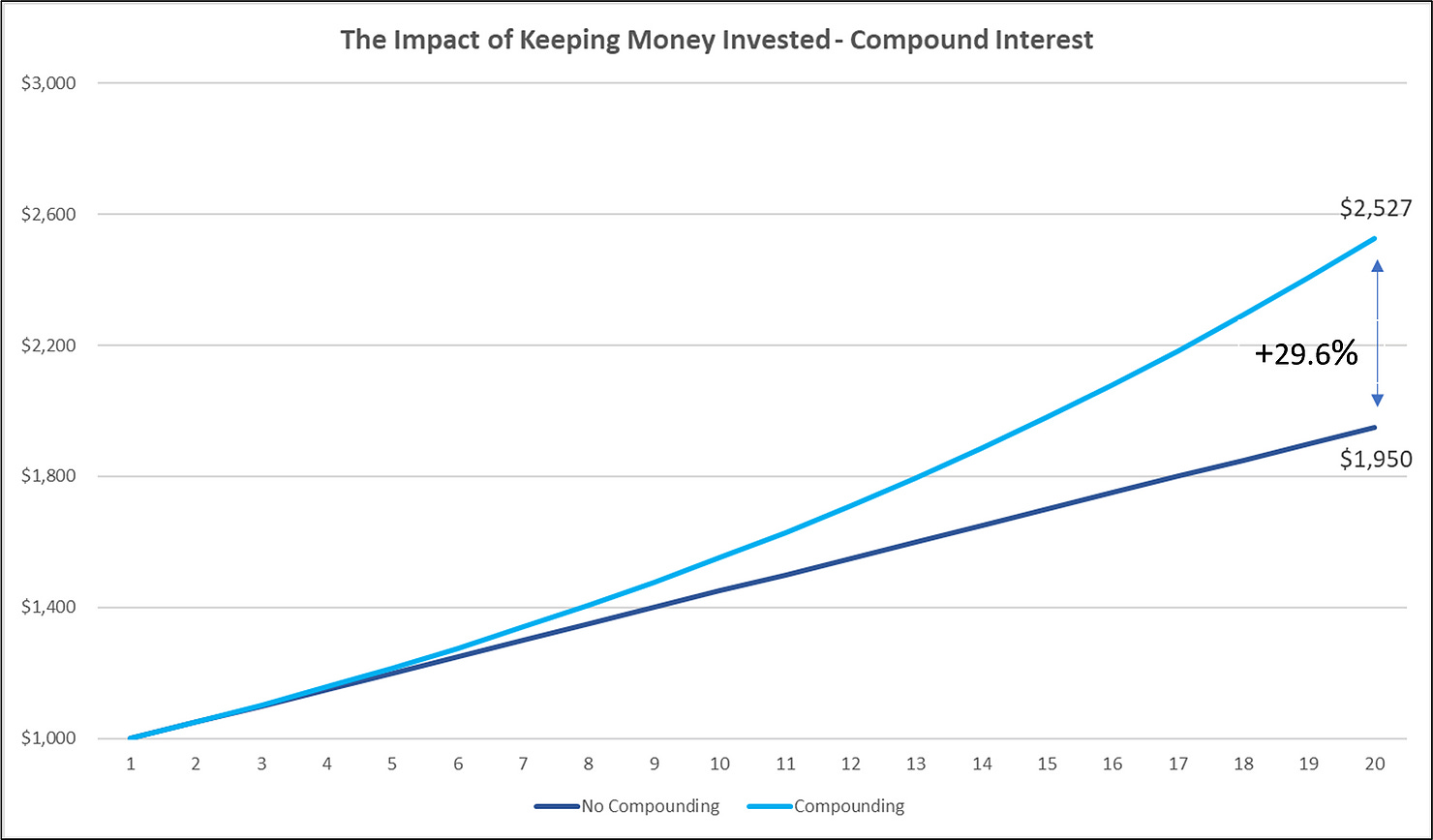

What is it? Put simply, you earn interest on your interest. In other words, when you save you earn interest, growing your savings. The next interest payment is then calculated based on your initial amount plus the interest you already earned, and thus your interest payments get larger with each payment. This one is best illustrated with an example:

Say you start off with $1,000, and each year you earn %5. At the end of that 1st year, you'll have earned $50, and your account will be worth $1,050. In year 2, and this is the important part, instead of earning interest on $1,000, you now earn interest on $1,050. So in year 2, you earn 5% on $1,050, which is $52.50. So the longer you save and allow your money to grow, the more it actually grows over time!

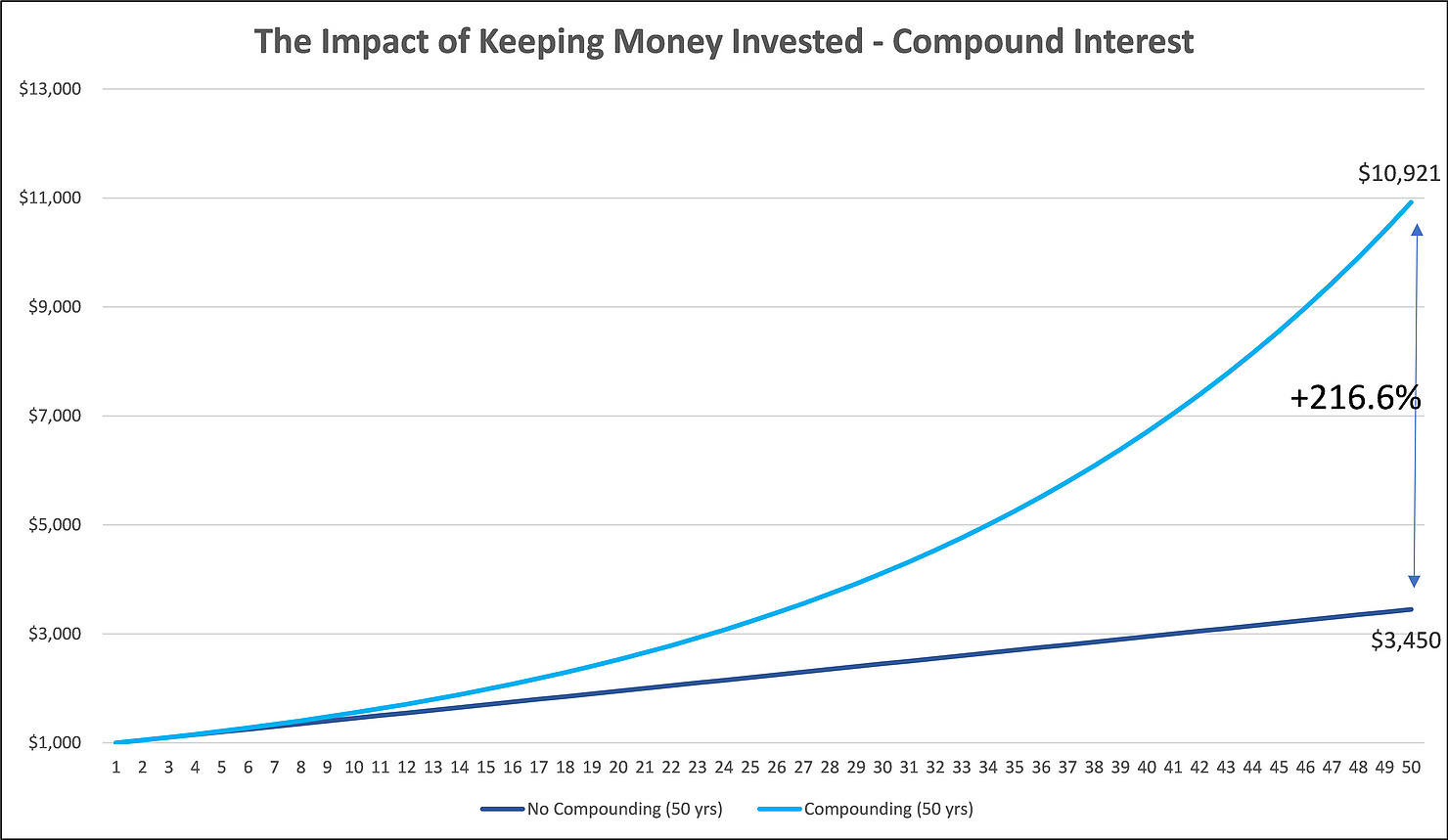

To further this point using the above example, over a 20 year period, compound interest results in a 30% larger gain vs. earning interest on your original amount alone. Also, notice how the compounding line gets steeper over time - this demonstrates how compound interest results in your money actually growing more as the amounts get bigger. To really hammer this home, look at the second graph, which shows 50 years' worth of compounding. Notice how the line continues to get steeper over time as the effect of compounding grows…

So the main takeaways? 1) Invest as early as you can to reap the benefits of compound interest, because the more time your money has to grow, the larger the effects of compounding…TIME IS YOUR FRIEND 2) Don't touch the money in your savings! Taking money out limits the true power of compounding.

Number 3. Buy low, Sell high

What is it? The concept here is simple, and is as old as finance itself. All it means is when investing, a simple rule to follow is you want to buy assets when they are perceived as cheap, and sell them after they grow and become more valuable. Think buying Amazon in the early 2000's and selling it today. The complicated part, however, is determining when something is cheap and when something is overvalued. It's also crucial to judge whether the asset that is cheap will even become more valuable in the future at all.

How about some more details. Ok so, the above makes investing seem really simple, but there's a lot more involved here.

The idea behind “buy low, sell high” relates the nature of stock market cycles. Stock prices fluctuate based on many factors: world events, interest rates, a company’s earnings growth, the perceived risk of a stock, inflation, the economic strength of the market, and so on. The image below highlights how the S&P 500, an index that measures the 500 largest US companies, rises and falls over time (the grey bars highlight recessions). The strategy behind buying low and selling high relies on trying to time the market. Buying low means trying to determine when stocks have hit their bottom price and purchasing shares in the hope of them going up. Conversely, selling high relies on figuring out when the market has hit its peak. Once stocks have hit their maximum value, investors sell their shares and reap the rewards.

Number 4: Retirement savings

What is it? Simple - money you save and more importantly invest to support you during retirement. A savings account is great for an emergency fund or your next big purchase, but when it comes to retirement, it pays to invest and earn a higher return in order to grow your money so that you have enough to live off of once you're ready to hang up your work shoes. Or work boots, depending on your industry.

How should I go about it? There are 2 accounts that are available that were created specifically for retirement, and they offer benefits that you won't find in other accounts, so it's seriously in your best interest to use them.

401K Plan

How it works: Available through your employer only. Here's how it works in a nutshell. You contribute a percentage of each paycheck, say 5%, to a 401K account. Your employer will then match your contribution (i.e. whatever amount you put in, so will they), up to a certain amount, say 5%, as their way of supporting your retirement savings. Said another way, if you make $1,000 per paycheck and direct %5, or $50, of that to be put into your 401K account, your employer will also put $50 into your account as their way of matching your contribution. IMPORTANT - your employer will only match up to a certain percentage, meaning they will put it what you do, but only up to a certain amount. The word MATCH is key here because if they are willing to match up to 5% and you only contribute 3%, they will only give you 3%. What this means is if you don't take advantage of the full employer match, YOU ARE GIVING UP FREE MONEY!

Benefits: Besides the employer match element, 401K's also have a tax advantage to help your investments to grow. I won't get into a ton of detail here since the match can be a bit much, but in simple terms, you can defer the taxes on income and gains you make in this account, and that allows your investment to grow more quickly than if they were taxed now. An additional benefit is that there's a penalty for taking money out of this account before your 59.5 years old. I know what you're thinking…how is that a benefit? The benefit is that it limits the temptation to take this money out early, which gives you a better chance of having enough money for retirement.

IRA

How it works: This is the ideal account type for folks who don't have an employer that offers 401K benefits. It has many of the same qualities as a 401K plan, but without the employer match element.

Benefits: Similar to a 401K plan, an IRA offers tax benefits that help investments grow as well as penalties in some cases for withdrawing funds before your 59.5 years old.

Important things to know. Starting to save for retirement when you are young is critically important because of compound interest (discussed in Number 2). Since the intent of retirement accounts is to invest now and not touch this money for a long time, there's ample time for compound interest to work its magic. And as we've shown, compound interest's effect gets bigger with time (see the 2 charts under Number 2. Compound Interest).

Number 5. Don't Accumulate Credit

What is it? This rule is meant to say that you should be careful in taking on too much credit, specifically credit card debt. Credit cards when used prudently can be great tools for dealing with short term cash needs (e.g. I need groceries now, but I get paid next week), building up your credit score (discussed under Number 10), and in some cases offer rewards for spending that aren't found with debit cards, like cashback or reward points (DISCLAIMER - credit card rewards are great, but don't use them to justify spending more than you would without them). But when you take on too much credit card debt, there can be some real consequences.

Consequences of Too Much Credit Card Debt

The amount you owe can increase quickly. Here compound interest works against you. Credit cards have high-interest rates (often greater than 20%), and as you miss payments and this interest accumulates, the interest charges quickly get larger, making it harder and harder to pay off.

Your credit score could suffer. Using too much of your credit card limit and/or missing payments will hurt your credit score, which will hurt your ability to get future credit cards and other loans (discussed more under Number 10).

Number 6. Diversification is Key for Mitigating your Risks

What is it? The official-sounding definition - Diversification is a risk management strategy that mixes a wide variety of investments within a portfolio. A diversified portfolio contains a mix of distinct asset types in an attempt at limiting exposure to any single asset or risk. In simple terms - Diversification can be understood as "Don't put all your eggs in one basket". While a single investment could do really well and make you rich, it could also make you broke. By allocating your money among different assets and investments, a.k.a. diversifying, you limit your exposure to a particular risk/investment/company. A key element of diversification is making uncorrelated investments, meaning investments that don't share the same risk factors. For example, if all your investments are in real estate and the real estate market tanks, your beat. But when real estate crashes, technology companies might do well, and so having a mix of investments across multiple asset classes (think stocks and bonds), sectors (think real estate, technology, and energy), and geographies (US, China, the EU) will help to grow your money while limiting extreme losses.

How should I go about it? Diversification, great concept right? But how do you actually implement it in your investments in an easy and effective way? This is where mutual funds and ETF's shine.

Mutual Funds: Basically, a mutual fund is an investment vehicle that pools money from many investors (hence why they're called "mutual") and invests it on their behalf according to the fund's investment focus (maybe the fund specializes in stocks, bonds, commodities, etc.). It is managed professionally by a portfolio manager who makes the investment decisions for the fund and monitors it to make changes as economic conditions change.

ETF's: ETF stands for Exchange Traded Fund, and it's very similar in nature to a mutual fund with a few notable differences. 1) While most mutual funds make investments in order to beat a benchmark (for example, a mutual fund that invests in large US companies and tries to outperform the S&P 500 Index, which tracks the performance of the 500 largest companies in the US), an ETF simply tracks an index, such as the S&P 500. So for example, an ETF that tracks the S&P 500 index will invest in all (or most) of the companies in the index in order to match its performance. 2) ETF's are cheaper than Mutual Funds. This is because while a portfolio manager is actively making investment decisions in order to try and beat a benchmark, the tracking-only nature of ETF's means there's less decision making, and thus lower fees. Note - investors need to weigh the cost of mutual funds vs. their ability to outperform their benchmark. The fact is that many mutual funds fail to outperform their benchmark, thus making ETF's that track the same benchmark a better option in many cases.

Final Takeaways

While investing all your money into Amazon in the '90s would have made you rich, in reality, it's extremely hard to tell if a company is going to do well over time. For this reason, it's important to hold a series of investments that are uncorrelated with each other in order to limit the risk in the portfolio.

Diversifying might limit your upside (again, investing in a single company might make you more, but it could also wipe you out), but over the long-term, it's a reliable way to grow your money and limit extreme losses.

Mutual Funds and ETF's are an extremely effective and cheap way to build a diversified portfolio. The other option is to do your own extensive research on all the companies that exist and to constantly monitor news on them and the global economy in the hopes of making better investment choices than professional money managers…I think you know the better choice ;)

Number 7. Keep your Savings and your Checkings Completely Separated

What does it mean? This one is simple, and important. Keep your spending money separate from your savings. Let's be honest, spending money is way easier than saving it, and when you have all of your money in a single account, you're more likely to spend it.

So what should you do? Keep that sh@t separate! Some easy yet effective ways to do this:

Have accounts that are completely separate (duh!). My advice - have an account at two different banks. Have one that is for savings only, and have absolutely no credit or debit cards, bills, subscriptions, etc. linked to it. This means to access your savings money, it will take a lot of effort. And that simple fact alone means you're way less likely to spend it.

Automate! This is easiest when your paychecks come in as direct deposits. Your employer should allow you to pick more than one account to deposit your checks in, and you can specify the % that goes to each. This allows you to pick a % of your check that will automatically be sent to your savings account. And this automation alone will make saving 10x easier and counters our natural propensity to spend.

Sounds great, but how much should I save? Great question, and at the expense of sounding cliché, it all depends on your unique circumstances. A good goal to aim is for is 20% of your pay.

Number 8. Debt makes the good times great and the bad times worse (be careful when you invest with margin)

What the hell are you talking about? Simply put, margin is money you borrow in order to make an investment (such as buying a stock).

Got it. And why do people do this? In a nutshell, borrowing money to invest has the potential to enhance your returns. Here's a quick demonstration: If you invest $100 in an investment that earns $10, then you've made 10% on your investment (10/100 = 10%). Now, say you make the same investment except this time you only invest $50 of your own money and borrow the other $50. If the investment earns $10, the return you make on the money you invest is now roughly 20% (10/50 = 20%, minus the interest you pay on the loan). So using margin has the ability to enhance your returns.

Sounds awesome…why not just do this for every investment? Good question. Margin is great when the investment works out, but what about when it doesn’t? Using the same example above, a $100 investment that loses $10 results in a 10% loss. This same investment bought 50/50 with your own money and margin would result in a 20% loss (-10/50 = -20%), plus, you still need to pay back the loan and interest. To make matters worse, margin calls (essentially the lender requesting you to put more money in your account to support the loan) can result in your assets being sold at undesirable prices in order for the lender to get their money back, which means you miss out on any recovery in the value of the investment. Picture having to sell your assets when the market fell during the first month of the COVID-19 only to see it come all the way back a few months later…ouch!

So what should I do? My opinion? Stay away from it unless you really, and I mean really, know what you're doing. It sounds fun, until it isn't.

Number 9. Past Performance isn't a Guarantee of Future Results

What's it mean? This one's pretty straightforward, and a lesson we can see playing out well outside of investing. Star college athletes underperforming once they get to the pros, that reliable family car suddenly breaking down, or that crush you had who answered all of your texts and then suddenly starts ghosting you…The lesson in this is that the past doesn't dictate the future. And when it comes to investments, just because something did well in the past doesn’t mean it's going to continue to do so. The classic example of this is buying a stock because it's had a good stretch and you're hoping it continues.

So then what should I do? Do your research. Ask yourself if you're buying something simply because it did well before, or because you've done your homework, you understand the strategy of the company, and you believe they will do better than their competition going forward.

Number 10. Credit Score

The term everyone's heard, but few understand. Talk to me, please. Ok so, people who lend you money need a way to measure the risk of you not paying them back. Say hello to the credit score. It's used when getting a mortgage, a car loan, a credit card, and is even used by employers making decisions about hiring and landlords approving tenants. Needless to say, it's important.

Damn, good to know. But how do they calculate this thing? There's a lot that goes into it, but 5 of the main factors, in order of importance, are 1) Payment History - do you pay your bills on time 2) Credit Utilization - how much debt do you have relative to your credit limit - using more of your limit implies a higher dependency on credit, which is bad 3) Length of Credit History - a longer history of credit gives lenders more information to assess you on, and the longer you pay bills on time, the better 4) Inquiries - how many credit checks you receive - too many can mean you are taking on a lot of debt and are possibly in financial distress 5) Mix of Credit - having different kinds of accounts is favorable because it shows you can handle managing an array of credit types (mortgage, credit card, auto, etc.).

Sounds good, but, how do I know if my score is good or bad? Here's a simple list with some ranges:

- 750 or higher – Excellent

- 700 to 749 – Good

- 650 to 699 – Fair

- 600 to 649 – Poor

- Below 600 – Extremely Poor

Great, I'm in the lower bracket. What can I do to move up? Now you're asking the right questions! Some simples tips are 1) pay your bills on time (duh!) 2) lower your utilization rate - if you have a $15k limit on your credit card, only use a low amount, say 10% 3) If you have a limited credit history, you can use on-time utility and cell phone payments to demonstrate your creditworthiness 4) only apply for and open new credit accounts as needed - too many accounts can lead to too many inquiries and tempt you into spending too much 5) make sure you dispute any errors on your score (which you can check online), as getting these removed can help boost your score.

I hope this has helped you get a better understanding of some of the basic principles of personal finance that can help you become more financially secure. Please leave a comment with your thoughts and or questions! Links are below to share if you know others who may benefit from this piece.

Want more content like this? Sign up for our newsletter to get exclusive content and tips!